A SEBI Registered Investment Advisor is authorized and regulated by SEBI (Securities and Exchange Board of India) to provide investment advice in an unbiased manner. They operate on a fee-based model, and do not get any compensation from any of the investment product manufacturers. If you do not have the knowledge or the time required to choose your own investments, the safest way to invest would be to consult a SEBI Registered Investment Advisor instead of falling for the sales pitch of a product seller or distributor.

A Registered Investment Advisor comes directly under the regulations of SEBI and is expected to act as a client fiduciary and hence is bound to keep all information confidential. However, you may insist on signing a Non Disclosure Agreement (NDA) to ensure some legal sanctity as well.

It is always advisable to keep the implementation of investments separate from the person who provides the investment advice. This ensures that the advice provided is truly independent of any monetary incentives from the product manufacturers. Even mutual funds provide ‘Direct Plans’ which does not engage any agent and can be directly implemented upon the advice received from a SEBI RIA. Even for investments directly in the share markets, there are reputed online discount brokers who charge a flat fee per transaction instead of a percentage of the transaction amount. Such options will save you huge amounts of money in operational expenses in the long run.

Some advisors may have their family members involved in distribution of investment products, and if the advisor insists on implementing the recommendations with them, you may excuse yourself from doing so and choose the direct mode.

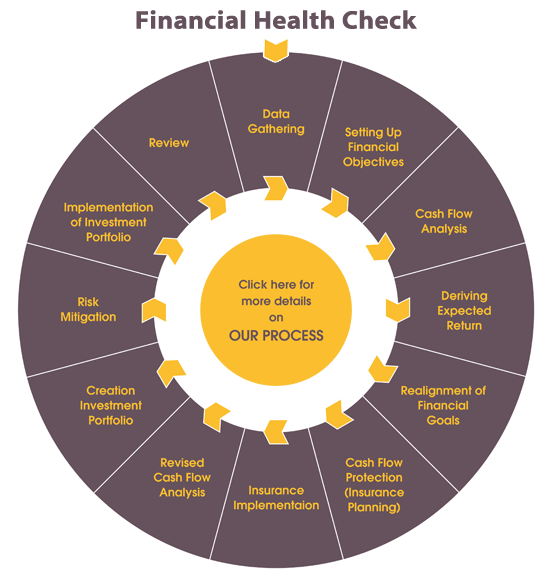

No advisor can (nor is supposed to) provide any guarantees on the recommended investments as they are subject to market vagaries. It would pay you well to understand that even bank deposits are safe only to the extent of ₹1 Lakh through the insurance scheme of the Government of India! Therefore, you need to understand that the investments made require your patience to deliver performance. The key to successful investment is to know the risks involved and create a diversified investment portfolio spread across various asset classes as per your financial strategy determined through the Life Cash Flow Analysis and Feasibility Study of various goals. You may insist that your investment advisor takes you through this process before recommending the investments!

I am too young / old While it is true that the younger you start the more beneficial the process will be, financial planning is worthwhile at any age. Although younger people may have more decisions to make regarding their financial lives, changing laws and circumstances can lead middle-aged people and seniors to have to adjust their financial plans as well. Changes in tax law, for example, may require many people to revisit certain investments or estate plans, and adequate disability planning becomes more important as people age. I save enough How much is enough can only be determined after you do your need analysis in a scientific manner? I have enough assets to take care of my needs What is termed as an asset is itself a debatable issue, however generally an 'Asset' is "what produces an income for the holder." And if left unmonitored assets could lose its value due to market forces and may be insufficient to fulfill the needs when they arise. I can always borrow when I need Borrowing of money depends on various parameters such as interest rates, repayment capacity and eligibility which may change from time to time and is independent of the timing of requirement. Therefore complete dependency on borrowing is not recommended. I don't need to think about retirement, my kids will take care of me Every individual has his/her own priorities which are more or less decided by circumstances. In such a scenario, it is always advisable to build the nest before it rains instead of depending on someone else, even if that someone is your own child. My business will take care of me Business is one of the most volatile sources of income. There are many governing factors such as recession and liquidity in the market which could adversely affect the profitability of a business. Therefore it is recommended to avoid excessive dependency on one's own business and create a parallel passive source of income through an appropriate investment portfolio sufficient enough to provide for the financial goals. I do enough investments to save tax Investing to save tax is the most popular practice prevailing in India. No doubt that is one of the strategies of tax planning. However, many a times such investments are done without analyzing the instrument or the financial objective. My business will always be profitable, so I reinvest all my income into my own business As the old adage says, don't put all your eggs in one basket even if the basket is your own!! Therefore reinvestment into one's own business should be after budgeting for creation of an appropriate investment portfolio sufficient enough to provide for the financial goals on a year on year basis and also after taking into consideration one's life stage. I'll always have my job In the current economic situation, job security is a very distant dream. Almost surely you would get another job, however, there is no guarantee of similar income being replaced in the new assignment and what about the period in between these jobs when there is no income and only expenses? Would you be able to sustain your current lifestyle? I am insured Insurance is just one aspect of financial planning. In addition to checking whether you are adequately insured in a scientific manner, we should also take care of the various financial goals in a systematic way by making sure that adequate cash flows are available at the right time.

An ideal financial planner is expected to be totally unbiased towards the client. However you may judge his genuineness by the certification he possesses and by his method of remuneration i.e. fees or commission. A financial planner who provides fee based service is almost always unbiased, because he is not dependent on making money through commission from the investments made, and therefore solutions provided would most probably be in your best interest.

Some personal finance software packages, magazines or self-help books can help you do your own financial planning. However, you may decide to seek help from a professional financial planner if:

You are the focus of the financial planning process. As such, the results you get from working with a financial planner are as much your responsibility as they are those of the planner. To achieve the best results from your financial planning engagement, you will need to be prepared to avoid some of the common mistakes by considering the following advice:

+91-8007480300

+91-8007480300