Team Horus strongly believes that their approach would eventually play a vital role in creating a financially aware society by helping it develop a HEALTHY ATTITUDE towards MONEY! i.e. To treat money as a tool to create peace of mind rather than being enslaved by it.

Currently, Horus has moved ahead of the times and is not just a training centre for CERTIFIED FINANCIAL PLANNER program but has been conceived as a finishing school i.e. an end to end coaching organization for for aspiring financial planning practitioners.

This is a conducive ecosystem for new financial planners who would be supported and guided by senior financial planners to set up their clientele for financial planning by offering a well established, scientific and structured financial planning process. They are also exposed to on going training programs through which their knowledge levels are updated and made relevant. Further they get to participate in a lot of corporate interventions through which they come across the appropriate target clients. This approach of coaching which involves the domain as well as professional aspects and continuing guidance by senior financial planners enables the associates of Horus to provide a high quality, unbiased financial planning service to their clients, instead of just being another insurance/ mutual fund agent or a product seller!

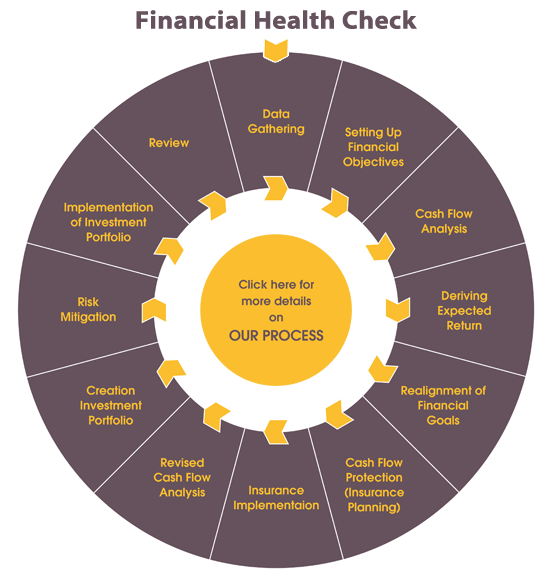

Data gathering means collection of information relevant to the financial planning process. In this step, a financial planner collects information about the client’s financial goals, income, expenditure, investments etc. This is the first step in actual financial plan preparation & it plays a foundational role in construction of a financial plan. Success of a financial plan wholly depends on the given data and to make sure that the data given is accurate is solely the client’s responsibility.

This is the second step in financial plan construction process and in this process a financial planner converts the needs and aspirations of the client into tangible numbers, especially the quantity of money required at various stages for each goal such as retirement, children's education, marriage, purchase of new house/car, foreign tours etc.

Once the Financial Objectives are set up, all the cash inflows and outflows (both current and projected future cash flows) are mapped on to a worksheet and detailed analysis is done in order to derive the expected return on investment of surpluses generated in each year. There could be two outputs for this exercise.

Once the expected return on investments/ expected income is derived, and if it falls beyond the acceptable criteria, it means that some of the goals are beyond reach as on date and should be either postponed or ‘cancelled for the time being’. If any goal is cancelled, it could find its way back into the system at the time of review or whenever cash flows change substantially in the positive direction. Multiple scenarios involving re-alignment of various goals could be looked at before making the final decision.

The financial plan is heavily dependent on two factors.

Therefore careful consideration has to be taken in order to protect these factors in the event of occurrence of an unfortunate incident such as death, disability, theft, fire, natural calamities etc. This is ensured through adequate Insurance planning for all assets (Life, Health, Property etc.) For health and property, it is a very simple exercise to compute the amount of insurance since their monetary values are readily available.

eg: A house can be insured to the extent of ‘cost of reconstruction’ in the event it gets destroyed completely Health can be insured to the extent of the cost of treatment for various ailments/surgeries with sufficient allowances based on the health history of the individual/family.

However it is impossible to determine an appropriate value in the case of Life Insurance as there cannot be a monetary value attributed to human life! Therefore we need to resort to some complex methods using some alternative logic as given below:

This approach looks into the financial goals set by the individual in the order of priority and filters out those objectives which have to be accomplished irrespective of whether the person concerned is alive or not. These filtered goal values are used for estimation of insurance requirement.Further optimization can be done in this approach by using our unique method of ‘Life Insurance Laddering’ Since this method gives a very realistic and efficient estimate of life insurance requirement, it is used in our Comprehensive Financial Planning engagement.

This uses the income generated by the individual as a benchmark for insurance calculation. However this method may not give us a realistic estimate in certain extreme cases and therefore is considered to be inefficient. Therefore we use this method only in the 2 hour Financial Health Check engagement, where we have to estimate the insurance requirement in a quick fire manner and that too with limited data.

The insurance premium is considered as a cost/expense by us and NOT as an investment since we recommend pure risk coverage products only as they are the most efficient and excellent value for money. Now, since we use the ‘Need based approach’ for life insurance computation, the Cash flow analysis has to precede the insurance calculation and therefore the costs relating to fresh insurance implementation could not be factored into the cash flow analysis. Further, there is a possibility of the actual premium being different from the indicative value owing primarily to the medical condition of the individual. This presents a catch 22 situation. The only way out is to repeat the cash flow analysis step after incorporating the fresh insurance costs! The result of this step is the ‘revised expected return’, which will be used to prepare the investment portfolio.

Once the required rate of return is known, a financial planner would be in a better position to create an appropriate investment portfolio. This is the reason why contrary to popular belief, financial planning is NOT about ‘dealing with investments’. It is more of a philosophy and process, which, if practiced would give a more logical, realistic and consistent result. Very few people understand this, though! The major challenge in this step is to ensure an appropriate spread across various asset classes without hampering the expected return! Also care needs to be taken to choose the most optimum combination which gives the least measurement of risk in without hampering the balance in the asset allocation! This interplay between return, risk and asset allocation is the sensitive balance that has to be maintained on a continuous basis which cannot be achieved without in depth study

Once the portfolio is made, it is highly recommended that it be re-balanced on a yearly basis, taking cognizance of the realized return during the year and the changes in the cash flow pattern of the individual.

The process so far has been only a blue print of your financial plan and will bear fruits only if it gets translated into reality in terms of actually investing the recommended amount of money in the respective asset classes. Further, care has to be taken with respect to the proportions of investments suggested across the various assets within an asset class. Though we recommend investments in fixed income instruments such as NSE, PPF or FD to be made in the lump sum mode, investments into variable income instruments such as direct equity, mutual funds etc has to be done in a phase wise manner so that the market fluctuations could be taken advantage of. Our specialty in this step is that specific recommendations would be given from our end in terms of what portion of the variable income instruments should be invested from time to time and we call this ‘Market Sensitive Implementation Strategy’. This generally gets compared with a systematic investment plan. However the truth is that though it looks similar, the major difference between the two strategies is that SIP is a passive strategy and MSIS is an active strategy incorporating continuous market intelligence based on local and global economic factors. Simply put, since it is difficult to time the market at the lowest level with a large amount, we’ll try to time the market at every dip during the market cycle with small amounts.

A financial plan can be humorously described as a continuous battle between futuristic projection and accomplished reality!

Therefore it is highly recommended that the whole process may be repeated at regular intervals (generally in an annual mode) to take cognizance of the difference between the winner and the loser. If the accomplished reality is the victor, then the investment strategy for the next year would shift towards a more conservative side and in case it is the loser, a more aggressive stance would be taken.

The deviations between expected and realized values could occur primarily in the cash flows, goals and the investment returns. This would have a secondary impact on the expected return for the next year, insurance requirements and the composition of the investment portfolio. It may sometimes happen that the changes happen anywhere during the year before the regular review becomes due. In such a scenario, the client can initiate what we call as an ‘Accelerated Review’. There are no restrictions on the number of accelerated reviews during the year provided the reasons cited are genuine and could have a substantial impact on the financial plan.

To create and sustain awareness about the need of comprehensive financial planning to a large cross section of the society, through coaching aspiring

financial planning practitioners who would inturn help people to evaluate and

select the various investment tools as per their needs, and protect them from making irrational financial decisions.

Chenthil has been in the Financial Services industry for the past 15 years. From 2007 to 2013, he was coaching individuals for the internationally recognized Certified Financial Planner certification, in association with Indian School Of Business & Finance, an approved education provider with Financial Planning Standards Board, India.

Over the years he has gained a deeper understanding of human behaviour and responses when it comes to taking financial decisions and also about their ignorance with regard to managing their money.

This led him to author his first book “Everyone Has an Eye on Your Wallet! Do You?” which is quite exhaustive and provides directions for laymen and seasoned investors alike to take charge of their finances.

His vision for Horus when he founded it in 2009 was to be a finishing school for aspiring financial planners and has coached and helped many of them to set up their own practice. He is currently leading it into the FinTech space - more specifically the Hybrid Financial Advisory space which is a beautiful combination of aggressive expansion through AI based Robot Advisory and consolidation through creating an army of unbiased financial planners.

His corporate interventions include awareness programs and training assignments that help people lead better financial lives.

The topics in these sessions range from Basic Financial Planning Process to Wealth Creation and Behavioral Finance.

Teaching being his natural passion, he has done a few guest-lectures in management schools such as MIT school of management, Symbiosis, Times Pro-Learning etc.

He has been featured in various news papers and magazines such as Economic Times, Hindustan Times, Outlook Money & Financial Planning Journal.

He has also been a panelist for the pre-budget round table aired by newsX channel in association with BW Business world magazine.

With over 5 years of dedicated experience in the financial services industry,

Nikkhiel brings professional expertise and personal commitment to every client relationship. As a NISM-certified Investment Advisor, he combines technical knowledge with a genuine passion for helping others achieve their financial goals. Having witnessed the impact of financial misinformation and predatory practices firsthand during his corporate career, Nikkhiel transformed his passion for financial literacy into a mission-driven practice.

His transition from successful corporate professional to independent financial strategist was driven by a deep commitment towards fostering financial wellness in our community.

Nikkhiel is an engineer from Pune University & also an MBA from Symbiosis Institute of Business Management (SIBM), Pune.

Rohan brings over 7 years of experience in the financial services industry, backed by a deep passion for improving financial awareness and empowering individuals to take charge of their financial lives.As a Chartered Wealth Manager®, he combines technical knowledge with a client-first mindset to support confident, well-informed decision-making.

At Horus Financial Consultants Pvt. Ltd., he has conducted online awareness sessions and worked with many individuals and families, helping them understand their finances better and take meaningful steps toward their goals. Rohan’s journey into finance began out of genuine interest and a desire to make a difference. Starting as a structural engineer, he later followed his passion for personal finance and went on to work in various roles such as Equity Analyst and Financial Strategist, staying committed to making finance simple, effective, and accessible.

Horus was founded in the year 2009, with the sole intention of being a finishing school for aspiring financial planners, who wish to set up their practise and deliver unbiased advice to their clients. In my experience of close to a decade and a half, I have noticed that there is a pent up demand for unbiased advisors who can grow to become a trusted family friend of their clients and can act without any hidden monetary motivation. This is because most of the financial intermediaries work on a commission basis and have a tendency to sell the product that gives them the maximum remuneration.

That does not mean that the advisor shouldn’t be paid! The only way out of this situation is to create a new league of financial planners who work on a fee based model. In my view, the advisor, or in Horus parlance the Strategist, should have a well rounded philosophy and process which can command the respect of prospective clients and in turn be in a position to charge a suitable fee directly from them for the value delivered. Creating these strategists and providing them with the required infrastructure and support is the sole idea for which Horus exists.

Setting up one’s practise is solely based on one’s passion and knowledge. To address this we have created a comprehensive training module which covers not only the core concepts but also the practical application of these concepts through exposure to actual case studies and mini projects. The scope of the training extends to include development of interpersonal skills and overall personality which is vital to thrive in this industry.

However, scaling up is completely about leveraging technology. Keeping this in mind we have created our own financial planning software. This would help the strategists to complete the financial planning process within a small time frame, thereby helping them to accommodate more number of clients within the limited time available.

One message I wish to give all aspiring Financial Strategists is to NOT believe the cliché “Financial planning is at a nascent stage in India”. Raise your self- image and believe that if there is enough value on the table, the client will pay the adequate fee for your services! A lot of quality thought has gone into designing the Horus platform to ensure that you are able to put that value on the table and I would sincerely advice you to check out this opportunity fully.

Opportunities at Horus are as limitless as the boundaries of your imagination. We're growing all the time and wherever we go and whatever we do, our people grow with us. We give talented and innovative individuals the chance to explore varied career paths in a challenging and rewarding professional environment.

To contribute and be a part of our Growth Plan, drop in your CV with a letter for the position you are applying for at careers@horusfinancials.com

+91-8007480300

+91-8007480300