+91-8007480300

+91-8007480300

Let me start with a small story. Two friends went for a picnic in the jungle. After a long and tiring walk they were relaxing by a brook side, when they heard the roar of a tiger. One of the friends started running right away while the other took some time to put on his shoes. Seeing this, his friend said while continuing to run. 'You fool, you can't run faster than the tiger by putting on a pair of shoes!'. On this he replied, 'I don't need to run faster than the tiger, but I definitely need to run faster than you!!'.

In real life, 'Change'is the tiger and in order to tackle it we need to be equipped with the right tools and escape deeply entrenched paradigms. Professional financial planning is one such change which is gradually picking up momentum in our country and only those who are prepared with the right kind of knowledge and attitude can survive in this industry. In this transitional phase, a very common question asked by financial planners is 'Should I charge a fee for my financial planning service or depend on commissions?'. This question can have many interpretations: One of these could be 'Is my service worth charging a fee?' This is purely a case of lack of self image, caused due to two reasons,

A. Lack of knowledge

B. Lack of confidence.

We shall deal with this in detail later.

Another interpretation of this question is 'The commissions look really lucrative. I may not be able to charge that much of fee upfront. What to do, I'm confused?'- This is a battle between the angel & demon inside of you! In this case, the person who asks the question wants an answer which he wants to hear and not what he needs to hear. A third interpretation could be 'I can't decide between the two, because I don't know what would be good for me'

And this is a classic: 'Should I meddle with something which is already working and risk everything in pursuit of change?!'

In all these scenarios, one can clearly see that it is 'me', 'me'and only 'me'underlying the thought process. In other words, it is a 'self centric'approach. Before I'm mistaken to be a saint, let me clarify. I'm not saying that you should not be self centric when it comes to your remuneration. All I am saying is that your remuneration should not interfere with the customer's need!

For example, if your revenue target from a client is ₹10000/-, and you have the following options, what would you choose?

Option 1 - You give him a financial solution which is most optimum with respect to his needs and charge a fee of ₹5000/-. Indirectly you get ₹5000/- as commissions through the products.

Option 2 - You are not ok with charging him a fee, so you give him a very rigid financial product which may not exactly mirror his needs but give you commissions worth ₹10000/-

Option 3 - You are not ok with charging a fee, but still you go with your conscience and give him the financial solution mentioned in option 1 and get commissions worth ₹5000/- only.

The option 3 looks very utopian and presents a lose - lose scenario because, the planner has to serve more number of clients to make the required amount of income and thereby the quality of service suffers. The planner also faces a sustainability crisis, since a low cost model like this requires the business to be highly scalable and that is very less in an advisory model in the current situation.

Among the other two, the choice is obvious, isn't it? In both cases your revenue target is being met; however in the first case the client's needs are not compromised upon.

So there is definitely a major shift required in the thought process, in terms of having a client centric approach, if you want to become a genuine financial planner. Need, instead of commissions should be the driving force behind product recommendations. The differential income expectation could be compensated by charging a suitable fee.

Now let us face the moment of truth and ask ourselves the question 'Is my service worth charging a fee?'

As mentioned before, it is but obvious that when the client writes a separate cheque towards your fee, he expects you to deliver more than a commission based product distributor. He does not know that a commission based product distributor may earn much more than the fee you may be charging by selling him the wrong products! This is a fact and we need to accept it in a very positive way. Tackling this would require a financial planner to have a high level of self image and this can only be achieved by keeping oneself abreast of the various happenings in the industry along with thorough knowledge on the basics of financial planning. The CFP certification definitely helps in this aspect. On a softer note, remember, you don't need to run faster than the tiger!

Let me give you a hypothetical situation. On your way home, a nicely dressed, well groomed, pleasant looking gentleman asks you for a lift. On the other hand, a shabbily dressed man with his mouth full of betel leaf or gutkha (of course, the stink goes without saying!) asks you for the same favor. Would the first man have an edge over the second? That's a no brainer, isn't it?

Dressing sharp, good grooming habits and smelling right go a long way to give you oodles of confidence, at the same time create the right impression on others. Occasionally though, it feels nice to ignore this and laze around but that would be a bad day to meet clients!

These are only the physical attributes. There are more important things which contribute to your posture. Frequent follow up with a prospective client for signing up for your financial planning engagement or purchase of the recommended products can irritate him no end. Keeping a safe distance with the client is an integral part of creating the right posture. Being punctual is one attribute I have been struggling with throughout my life due to my habit of cramming up my schedule. But the fact is that people definitely like others to be punctual, while they can easily forgive themselves if they give it a miss occasionally! So, a sure shot way to impress your clients is to respect his time and be punctual. This applies not only for the scheduled meetings, but also for the planning deadlines.

Primarily communication is language independent, though people confuse this word with command over English. Vicharon ka aadaan pradaan is what is called communication! If you can do this with a confident body language, language will never be a barrier. Having said that, I can't agree more with the fact that English is the simplest language to speak matters concerning finance. So, conscious effort needs to be put into learning English as well.

Another important word goes hand in hand with Communication. And that is 'Timely'. Too late or too early correspondences carry less, or no value at all. There are so many modern gadgets available in the market which would help you with timely communication, but I still put my bet on our good old daily planner in the physical form.

Nature rewards persistence. A human embryo takes full nine months to come out as a baby. A plant takes years to grow into a tree. After ages, thanks to 'mentos', human beings evolved from apes! What makes you think your financial planning practice is any different? Patience therefore, is of paramount importance. Patience with self, with family, with clients, with your bills, and the list goes on. You may want to quit your practice at times when a 'good job'comes calling. But you have to resist those temptations if you want the right practice to be set up and enjoy the flexibility and freedom. Easier said than done, you may say, and I fully agree!

'Selling', is an often misinterpreted word. Usages like 'selling shoe polish to a tribal'only make things worse! The word 'Salesman'almost always portrays the image of an individual infected with verbal diarrhea, trying his best to push something down your throat without even considering your need. Since 'Financial Planning'is nowhere close to this definition of 'Selling', I wish to use a new word for financial planning, 'Counseling'. The Webster's dictionary defines this word as quoted below...

"Professional guidance of the individual by utilizing psychological methods, especially in collecting case history data, using various techniques of the personal interview, and testing interests and aptitudes."

Let us analyze this definition in detail and try to fit it into the financial planning exercise.

Carrying or holding information does not necessarily translate into professional advice. 'Experts'give 'generalized opinions'based on the available information. However, a professional is supposed to give 'personalized recommendations', and not generalized opinions. During the financial planning exercise if the approach is client centric, the planner would be fully focused on the individual's needs and aspirations and his suggestions would be customized based on the specific information given by the individual, thereby making the whole exercise qualify as ' Professional guidance'.

In order to perform the financial planning process from a client centric approach, it is inevitable that the planner employs adequate interviewing and probing skills. Many a times, he may need to go in a little deeper into what the client said to fully decipher his requirements. Also at times it may be required that the planner gives him certain hints which enable him to tell more about his financial objectives or other data. The financial planner should also work on his people skills to effectively handle clients'objections regarding the remuneration model he proposes or the various techniques employed by him to draw out the financial plan. He should also be willing to patiently explain why a particular method was used to arrive at the required amount of insurance coverage or how a small change in the percentage holding of an asset class considerably reduced the risk of the portfolio.

In the process of interviewing the client for data gathering, adequate care needs to be taken to read between his speech, the various insecurities, degree of risk affinity, order of priorities etc which may not come explicitly during the conversation. This requires the planner to be extremely observant and alert during the data gathering exercise.

From the above description we could say conclusively that the process of client centric financial planning fits the definition of 'Counseling'word by word!

In short, instead of selling 'ideas'or 'products'to the clients, a professional financial planner should graduate himself completely into the role of an 'assistant buyer'for the client by developing and employing his counseling skills, in order to become truly and blissfully successful.

Individuals, who wish to create the right foundation for their financial planning practice, need to take special care in the process of 'Client Selection'. This is because of the fundamental difference between building a sales career and setting up of an advisory practice. Most of the people who are currently engaged in the financial services career, get remunerated through a transaction based brokerage. From the perspective of the nature of remuneration, it is nothing but a sales career, though their business cards talk about anything but sales! The mantra in a sales career is 'the more clients you have, the more products you sell and the more products you sell, the more money you make!'. This requires the person to reach out to new people every day to whom he could sell something to make a living. Anyone who has spent some years in this field would vouch for the fact that repeat sales from the same client cannot be depended upon for one's bread and butter. People generally consider repeat sales as bonus income. Trail and renewal commissions are the only face savers which bring some stability into the system. Since the whole arrangement is transaction based, it hardly matters who the client is. Any individual having surplus money to invest is welcome to be part of the clientele!

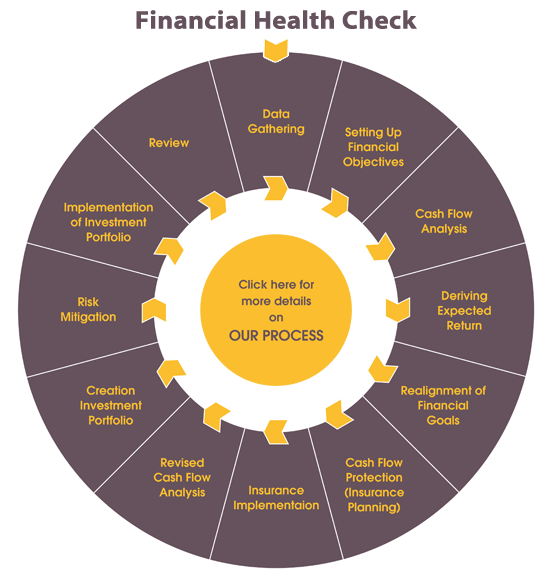

On the other hand, building a financial planning practice is very different from the system discussed above because of the design and structure of the entire process. FPSB's six step financial planning process starts with 'Establishing the client planner relationship'and ends with 'periodic monitoring and review'. Or does it end? No, it continues for a whole life time, which means you are going to give a slice of your life to a financial planning client! If one were to do a periodic review for each client, how many such clients can one serve in a satisfactory manner? 50, 100 or at the max 200, right? This is what brings about the necessity of carefully choosing the financial planning clients. However a distinct advantage of this type of engagement is that there would be a sustained and dependable income possibility through the review fee which could very well be 'inflation linked'!

Now, the million dollar question; how to go about 'Client Selection'? Here is a very handy tool. After the initial engagement with a prospective client, take out some time and go through the following check list. This is a bunch of close ended questions with Yes/No as answers and the respective scores alongside. Not much work to your grey cells!

A score of 10 or above surely qualifies the prospect to be worthy of being in your client team. However you may give a second chance to those who score 7 or above. But those with a score below 7 are strictly NO DEAL! Happy planning!!!

The wave of change has started devouring the first set of casualties in the mutual fund distributor network while major players are still figuring a way out. As is the usual case, most people are resisting the change. Many with whom I interacted with of late talk about this event with an uncomfortable excitement. Some of them are happy that the trail commissions are intact as the regulator has not touched the Fund Management Charges yet. But one thing is for sure; there is indeed a lot of chaos and confusion in the MF market. The insurance sector is also abuzz with rumors about the IRDA following suit with some regulations on insurance commissions.

On a positive note, regular investors in mutual funds who are happy with the service given by the distributors don't seem to be hesitant in shelling out some extra bucks to compensate the distributor.

For financial planners, the situation looks to be ideal to make the change over from commission based, to a fee based model. The environment is conducive for the investors also to make an attitude shift and willingly pay the right person for the right job for a hassle free financial future.

The bottom line is, whether you accept it or not, the change has struck. Those distributors who did not care to add value to themselves or their clients would most probably perish, and only those who were proactive would survive, when the dust settles. This kind of periodic filtering would only enhance the quality of financial advice in our country.

On the flip side, this event can bring about an increased focus on ULIPs from the selling fraternity. ULIPs, though they have their own unique features cannot be a substitute for mutual funds. But as the saying goes 'what is sold, gets bought!'. This could lead to a 'jumping from the frying pan to fire'kind of situation for unsuspecting clients who lack awareness about financial products and blindly believe their 'financial advisors'!

Subscribe Via Email

Subscribe to our mailing list to get the updates to your email inbox.