+91-8007480300

+91-8007480300

The financial planning profession is so exciting that I have found people jump into it without thinking twice. The perception of importance and respect associated with a financial planner vis-a-vis an agent selling financial products is so much that it is very easy to transform oneself mentally into this new avatar, in many cases, without properly internalizing the additional responsibilities that naturally come to a financial planner. A new born financial planner, in all sincerity and innocence thinks, 'I don't want to sound like an agent, trying to shove some products down the throat of a client. I want to be more dignified and think from the client's perspective, and don't mind losing some commissions in the bargain.' A couple of clients later, he starts feeling underpaid, because his benchmark of comparison is still that of an agent who made a killing selling a few insurance policies! More work and less pay!! More time invested with the client and less pay!!! More knowledge and less pay!!!! God, ignorance was truly bliss... This is what I call as "Hypothetical commission loss syndrome".

This is experienced by many new financial planners, who operate on commissions as their revenue stream. The solution to this issue lies in the shifting of one's core value from making quick money to setting up a proper financial planning practice. A commission earned through selling a financial product is by far the most uncomplicated way of earning revenue for a financial planner. There is easier acceptance from the client, a healthier, more frequent and sustainable cash flow (through renewal and trail commissions) and most importantly, one satisfied client leading to another through authentic referrals. Having said that, let us consider the flip side too. One of the main drawbacks in this system is the fact that you do not get paid upfront for your planning services. Your income lies in the client following through on your advice by actually investing in the suggested products, and that too through YOUR code or license! This amounts to expecting a high level of loyalty from the clients, which unfortunately is non- existent at least in your initial days as a financial planner. Also there is a risk of not getting adequately remunerated for your effort, since the commission rates are not directly proportional to your time investment. This again, may prompt you to suggest some solutions which attract more commissions to yourself, which may indirectly put the client to disadvantage, thereby defeating the very purpose of financial planning.

A way out to avoid such occurrences is to charge a nominal fee for your financial planning service. This way, your interests are kept right from the very beginning and you become immunized from the commissions derived from the suggested products, thereby enabling you to give unbiased solutions. Also, it can be easily validated that advisory professions such as teaching, accounting, medical practice etc. have been remunerated from time immemorial through a fee based model. What makes us financial planners any different? We are playing an advisory role to our clients and deserve to get compensated for our time through a nominal fee. The question here is 'what could be a nominal fee?' This can be worked out using a 4 step process.

The flip side in doing a fee based financial plan is that the prospective clients are not used to this kind of an arrangement, especially in India. People somehow think they are smarter than what they are, when it comes to financial matters. The only way to overcome the same, is through patient explanation of how paying a fee would enable the planner to give them an unbiased and efficient financial solution. Any new idea requires some effort to be put in order to become popular.

Some planners follow a combination approach, where their remuneration is evenly distributed between the fee charged and the commissions earned through the products. Though it looks like a nice idea incorporating the good things from both the methods, let us not forget that this also carries the flip sides of both!! So far we have discussed the various possible streams of revenue for a financial planner, where the planner gets paid for his efforts in reaching the implementation stage of the financial plan. However let me remind you that the biggest responsibility of a financial planner is yet to come; 'Periodic asset monitoring and review'!!

An initial financial plan invariably contains a lot of assumptions such as inflation, growth in income, size of the financial objective, the expected return, the risk profile of the client etc; the list may be very very long! This makes the periodic monitoring and review of the plan, the most critical aspect of the financial planning process. This in turn presents the financial planner the opportunity of creating a source of recurring revenue stream, the monitoring and review fee. This may be charged either as a flat fee or as a percentage of the total assets monitored. The planner may also decide to do the same in return for the commissions earned by him through the investments.

Now that we have discussed in detail, the different possible revenue streams of a financial planner, through all the stages of the financial planning process, it is time for us to attempt to arrive at an ideal combination of these methods, which would create a mutually productive situation for the two protagonists, the client and the planner. For this, let us first summarize the various parameters that are required to be considered.

1. The time invested by the planner

2. The absence of bias in the planner's mind while recommending solutions

3. The loyalty of the client and The commission rates in the prescribed solution.

Now, let us list down the various phases in which the planner adds value, for which he deserves remuneration.

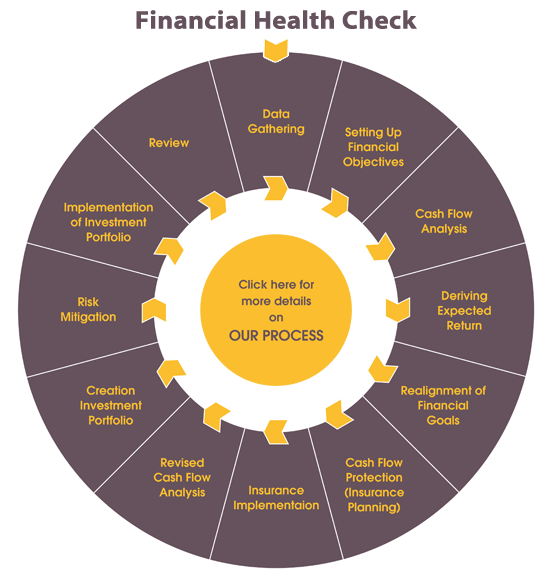

Phase 1 - Preparation and implementation of the Initial plan

Phase 2 - Periodic asset monitoring and review

It is evident from the above discussion that for being fair to the planner and to ensure that the client gets an unbiased solution, a fee based model would be ideal for phase 1. Some planners try to optimize the fee in this phase by offering to offset the same with the commissions earned through investments; however this offer would only confuse the client as he would not be in a position to attribute a specific value to the planner's effort.

By the time phase 1 is over, almost all the parameters listed above are taken care of. The time invested by the planner has been remunerated by the fee, which almost definitely eliminates the possibility of bias in the planner's mind. The client's loyalty is clearly known in terms of whether he has followed through with the recommendations made, and also by whether he has made the investments through the planner or not. If yes, the commissions earned through the solutions given is also known exactly.

This gives us some room for flexibility in phase 2, where the asset monitoring and review fee could very well be offset by the commissions earned, without causing any confusion to the client and also by being absolutely transparent with him. For example, if the asset monitoring and review fee at the end of one year happens to be ₹10000/- and you have already earned a commission of ₹6000/- through the investments made by the client in phase1, you may bill the client only ₹4000/- as the review fee. This way we can ensure fairness to both the parties in this professional engagement and there by create a long lasting, WIN-WIN relationship between them.

Happy planning!

Subscribe Via Email

Subscribe to our mailing list to get the updates to your email inbox.